Your 403(b) retirement plan is innovative because it offers you choices for planning your retirement. But when you look more closely at your employer-sponsored retirement plan, you may discover the illusion of choice—you may be able to choose where and how to direct your savings, but the range of investment options you must choose from are often limited.

Add to this problem that many of these options are poor to begin with—overexposed to risky sectors, rife with conflicts of interest, and returns that are too closely aligned to offer any diversification benefits.

If your 403(b) investment menu happens to include a small-cap, high-yield or other type of specialty fund, you probably get only one of these options. You have to take whatever investment options the plan offers—which is not really much of a choice.

The biggest risk a limited investment menu poses is the inability to control your destiny—you may be unable to manage your retirement savings in a way that suits your risk tolerance. The only choice you really have is to sit back and take what the market offers—the good, the bad, and worst of all, the really, really ugly in the form of catastrophic losses.

Unleash Your 403(b)

For example, you may not be aware of a different choice you may have for choosing investments for your 403(b) account, one that gives you flexibility in how you invest and allocate your retirement savings.

Today, many 403(b) plans offer more options to participants, whether by permitting you to work with your own financial advisor to manage your account or by opening access to a wider range of investment options through a brokerage window. Not every plan includes a brokerage window as an option, but those that do give participants a tremendous benefit you can use to take control of your destiny.

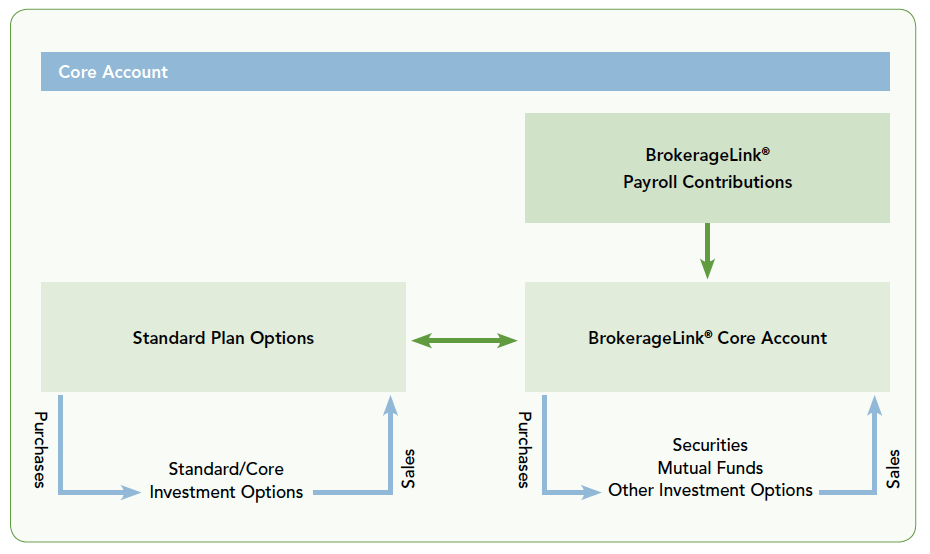

Fidelity is one of the largest providers of retirement plans to the 403(b) market. With their size and the scope of investment products available on their platform, they can offer 403(b) plans and participants a flexible brokerage window option called BrokerageLink®.

What is BrokerageLink®?

When included in a 403(b) plan, the brokerage window sits next to the investment lineup of standard plan options. You can choose one of two routes—either to allocate within the plan lineup of standard or core mutual funds, or to look to BrokerageLink® to build a portfolio from a wider range of options.

Source: Fidelity Investments. “An advisor’s guide to Fidelity BrokerageLink®”, 2017.

Also, don’t think of BrokerageLink® as a free-for-all. Your 403(b) plan may set “guard rails” on how you can use the platform. For example, your plan may limit what percentage of your retirement savings you can allocate to a BrokerageLink® account. Your 403(b) plan can also exclude certain securities or security types on BrokerageLink®, making them ineligible for investment.

Your 403(b) plan may also allow third-party advisors or portfolio managers to access the BrokerageLink® window to invest on your behalf. This is a crucial aspect because it’s important you get unbiased and personalized advice when making critical investment decisions that will impact your financial future.

Professional advice becomes even more important when you open the window to thousands of available options for allocating your retirement portfolio. With so many funds to pick from, it’s nearly impossible to do enough homework on each fund to make an informed investment decision. That’s part of the value that a financial advisor can bring to the brokerage window.

Of course, greater choice comes with greater responsibility. Anyone who’s lost track of time in the cereal aisle or searching for a movie on Netflix can appreciate how too many choices can lead to analysis paralysis. But when you choose to allocate your retirement portfolio through a brokerage window, you can also access objective advice offered by a financial advisor.

When the standard 403(b) plan menu doesn’t meet your needs, a financial advisor can help you navigate the expanded investment lineup. This is particularly useful if you want your investments to align with your financial goals and risk tolerance.

Success as an investor starts with understanding your risk tolerance and allocating your portfolio accordingly. We believe most investors do not understand what their true risk tolerance is—they can’t unless they ask themselves how much they are willing to lose in a market downturn.

This is a question that an effective financial advisor can help you answer. For our part, Potomac helps by asking the right questions to get the right answers. (And we designed our own risk tolerance questionnaire to do just that.)

Get started with BrokerageLink®

There are three simple steps to follow to start working with a financial advisor through Fidelity BrokerageLink®:

- Determine if your 403(b) plan will allow a financial advisor to help you: First you need to determine if your plan allows for advisor access and offers BrokerageLink®. To research this you can either call your Fidelity plan service center or provide your financial advisor a recent account statement.

- Completing the application process:

- The BrokerageLink® Application: You can register for an account online through your NetBenefits® login or complete an application in the BrokerageLink® kit. A financial advisor can walk you through this process to make sure it’s done correctly.

- Secure account access for third-party management by completing a few simple forms—In order to allow a financial advisor to manage your 403(b) account you will need to complete the Fidelity Registered Investment Advisor Authorization Form, the Registered Investment Advisor BrokerageLink® Authorization Form and any formal agreements required by your financial advisor. It’s 2018 so this should be able to be done electronically using DocuSign.

- Relax and let your advisor take it from here: Your advisor will work with you to determine the best investment strategy and take over the day to day responsibilities of managing your account.

What to Expect with Your New BrokerageLink® Account

Once you have your newly established BrokerageLink® account you will notice a few small changes. Not to worry, however, because your 403(b) account can still be accessed with the same NetBenefits login you have always used. Your financial advisor may also provide a client portal that will have a more in-depth account review including account and position level performance.

Not only will you see your total account value, but you will now have an asset titled “BrokerageLink” that will be the bulk of your account value.

Here are some helpful tips to keep in mind…

- A small portion of funds will be left on the plan side to cover any fees.

- Your plan will dictate how much money is allowed into BrokerageLink®, which in our experience is typically 90-100% of your account value.

- Your investment advisor will be able to handle moving the funds between your 403(b) account and the Brokeragelink® window as well as directing future contributions to be invested accordingly.

To see what funds you own in that BrokerageLink® window, you simply click on the BrokerageLink® asset listed and it will show you the fund allocations within your portfolio. You will continue to receive quarterly statements for your 403(b) account but in addition you will also receive monthly statements directly from Fidelity BrokerageLink®.

Fidelity, Potomac and You

Investing shouldn’t be a solo act —when you hire Potomac as an independent portfolio manager, we will offer guidance every step of the way.

We believe in the value that Fidelity BrokerageLink® brings to the table for individual investors like you. We’ve built our own architecture around BrokerageLink® to help us deploy our risk management strategies on your behalf.

When you partner with Potomac, you get personalized support from our team, who can help you take advantage of the opportunity to plan for a more secure financial future using your 403(b) plan and Fidelity BrokerageLink®.