With our expertise in the 403(b) market, we know the best way to help you grow your business in this space – is to arm you with tools that will add real value.

The following is guide designed to help your clients better understand and manage their 403(b) retirement plan, whether they are a new or experienced investor.

Your employer’s 403(b) retirement plan offers you the opportunity to save more of the money you earn and invest it for your financial future.

When you chose to invest through your employer’s 403(b) retirement plan, how you invested was entirely up to you. That could have been good or bad—good if you had a wide range of choices to help you invest in a way that suited your style and needs, but bad if you were new to investing or didn’t have time to research the options available in your plan.

A 403(b) is a retirement plan available to educational and health care institutions, in addition to certain non-profit organizations (police, firefighters, churches, etc.). A 403(b), also named after the section of the IRS code governing it, grows tax deferred until you begin to withdrawal from it at retirement. Plans that function similarly to a 403(b) but are named slightly different include: 401(a) and 457(b) plans.

Certain employees of tax-exempt organizations are eligible to participate. Participants include, but are not limited to, doctors, professors, nurses, teachers, ministers and administrators.

Like a 401(k), employees must work through their employer to setup and participate in their plan. Although the options can vary, employees execute a salary reduction agreement to make pre-tax contributions.

These contributions are then sent to custodians chosen by the employer such as Fidelity Investments. Contributions grow tax-deferred until the time of retirement, when withdrawals are taxed as ordinary income.

The History of the 403(b)

How did the 403(b) market get to where it is today? A look at the history of the 403(b) tells the story of its development.

403(b) plans predate 401(k)’s by over 20 years. In 1958, Congress passed the law that gave the IRS a green light to create tax-deferred savings accounts for employees at select non-profit organizations. (In comparison, 401(k) plans would not be launched until the early 1980s.) Three years after the 1958 law, eligibility for 403(b) plans was extended to workers in public schools and colleges.

403(b) annuities were the primary savings and investment vehicles in the early years of the 403(b) plan. Even before section 403(b) entered the Internal Revenue Code, annuities were used commonly by certain workers as a tax shelter to defer income, and likewise, their tax liability.

In fact, the impetus for the law creating 403(b) plans was to cap how much income workers could stash out of the IRS’s reach in tax-deferred annuity accounts. 403(b)’s weren’t meant to help people save for retirement; they were meant to

help the government capture tax revenue they had not been collecting.

The legacy of annuities as the primary 403(b) investment vehicle persists even today–you still see 403b plans referred to as “tax-sheltered annuities” or “TSAs”, leftover language from the earliest marketing efforts.

The market changed in 1974 when mutual funds were permitted for inclusion in 403(b) investment lineups. Mutual funds offered 403(b) participants diversified investment options, without the high sales and administrative fees common with annuities.

By 2013, 403(b) assets were split almost evenly between mutual funds and annuities, according to 403(b) filings in BrightScope’s defined contribution plan database.

Though 403(b) plans shared many similarities with their 401(k) brethren, the marketplace was much different for 403(b) providers and participants. For many years, it seemed like the Wild West–any 403(b) plan provider could send their sales reps into a school or a hospital, with minimal oversight from the school district or healthcare system.

Greedy salespeople sold inflexible and high cost annuities with little explanation to participants as to what they were buying or what fees they would pay.

Regulations Rock the 403(b) World

New regulations took effect in 2008 changing the 403(b) landscape. School districts, hospitals and any non-profit organization that wanted to sponsor 403(b) benefits now had to draft and comply with administrative plans.

Much like the plan documents required of 401(k) sponsors, these written rules would define eligibility requirements, contribution limits, investment selection and more for 403(b) plan participants.

The regulations transformed the 403(b) market to a structure that more closely resembled 401(k) plans. The new rules also would shrink the number of plan providers competing for 403(b) assets. There were fewer sharks in the water and not as many commission-hungry sales representatives chasing down doctors, nurses and teachers for their 403(b) contributions.

The 403(b) market became more efficient with these changes, but participants also saw fewer investment options directly on the plan side. However, many large plans opened brokerage windows for participants, giving them access to as many as 3,500 mutual funds to choose from.

Of course, so many choices have its advantages and disadvantages. A wide range of investment choices is great, but with all these choices how do participants decide?

Why Invest in Your 403(b) Retirement Plan?

Let’s start by answering an essential question you may have about your financial future—why invest at all?

The short answer is, you should invest because you can. Investing offers you a tremendous opportunity to put money you save to work for your future retirement needs. Think of it like getting a little extra money in your paycheck without having to work additional hours. Instead, your money works for you behind the scenes while you continue to work, allowing you to reap the rewards later.

The long answer is, you should invest because you must. That’s because money you earn today is worth more in the present than in the future because of inflation. This is a concept called the time value of money.

You can see a real-life example of this idea in the prices of many basic goods you purchase—for instance, a gallon of milk costs more today than it did 30 or 40 years ago and will likely cost more 30 or 40 years from now.

Inflation, as it is known, erodes the purchasing power of the money you save today so it won’t buy as much in the future. But you can counter the effects of inflation by seeking to grow your savings over time by investing it.

At the very least, you need to earn a return on your savings each year to match the annual inflation rate. That helps you break even by maintaining your money’s purchasing power.

One Easy Way to Grow Wealth

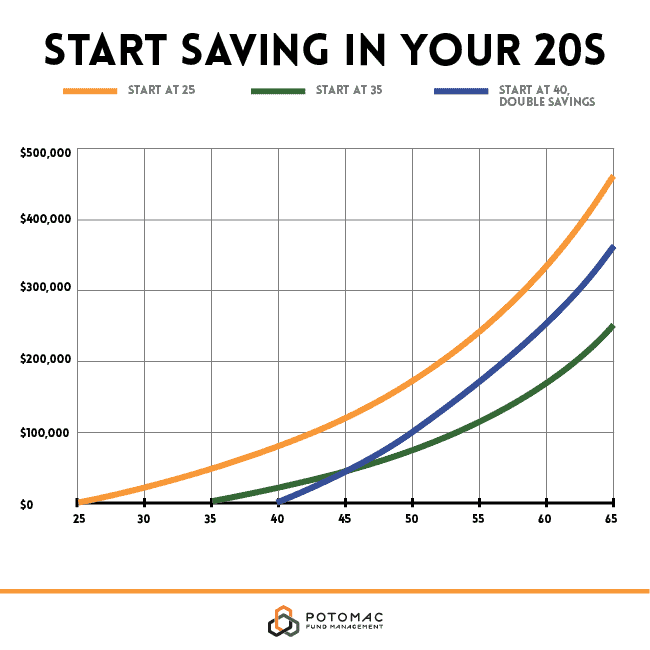

Money is one important component of investing, obviously. Another important component is time. The earlier you begin investing the greater your opportunity to grow your wealth. This is especially true when you put the power of compounding to work for your future.

Compounding is a simple concept—it involves putting the money you earn on your investments, whether it’s from price appreciation, income from dividends or interest you receive, back to work in the market. As you add earnings on top of earnings over time, the growth potential of your account multiplies.

Start Early to Make the Most of Time

The best time to start investing is when you’re young—even if you don’t earn that much yet and can save just a little of your paycheck, you still have time on your side. Compounding growth (especially on a tax-deferred basis in your 403(b) retirement plan) makes time a powerful force you can put to work for your financial future.

Your Path to a More Secure Financial Future

A 403(b) retirement plan is designed primarily to help you grow wealth for retirement. One of the biggest benefits you get by investing through your 403(b) is tax-deferred growth—any gains or earnings you realize on your investments won’t be taxed until you withdraw them. When tax-deferred growth and earnings stay in your 403(b) account, they can compound over time to help you accumulate greater wealth.

In general, you can tap your 403(b) for income starting at age 59½. Withdrawals before age 59½ are likely to be subject to penalties—that’s how the IRS directs that your 403(b) should be used to plan for retirement. All 403(b) money (contributions and earnings) will be taxed at your current personal income tax rate upon withdrawal.

The Major Benefits of Your 403(b) Plan

To begin, let’s highlight the major benefits available to you when you choose to open a 403(b) account:

- Contribution limits are very favorable for you, they come from your pre-tax earnings up to annual limits and are automatically deducted from your paycheck.

- Tax-deferred growth helps you keep and reinvest more of the money you earn on your investments.

- Several investment options from professional investment managers using pooled investment vehicles such as mutual funds.

Favorable Contribution Limits for 2018

You can contribute up to $19,000 of your pre-tax income to your 403(b) in 2018. If you’re over age 50, you can contribute an additional $6,000 in catch-up contributions. That raises your annual contribution limits to as much as $26,000 of pre-tax income.

All of these limits do change from year to year and details can be found on the IRS website.

Your employer may also offer matching contributions on top of what you contribute from your pay. The annual limit for combined contributions—your elective deferrals plus employer matches—is $55,000.

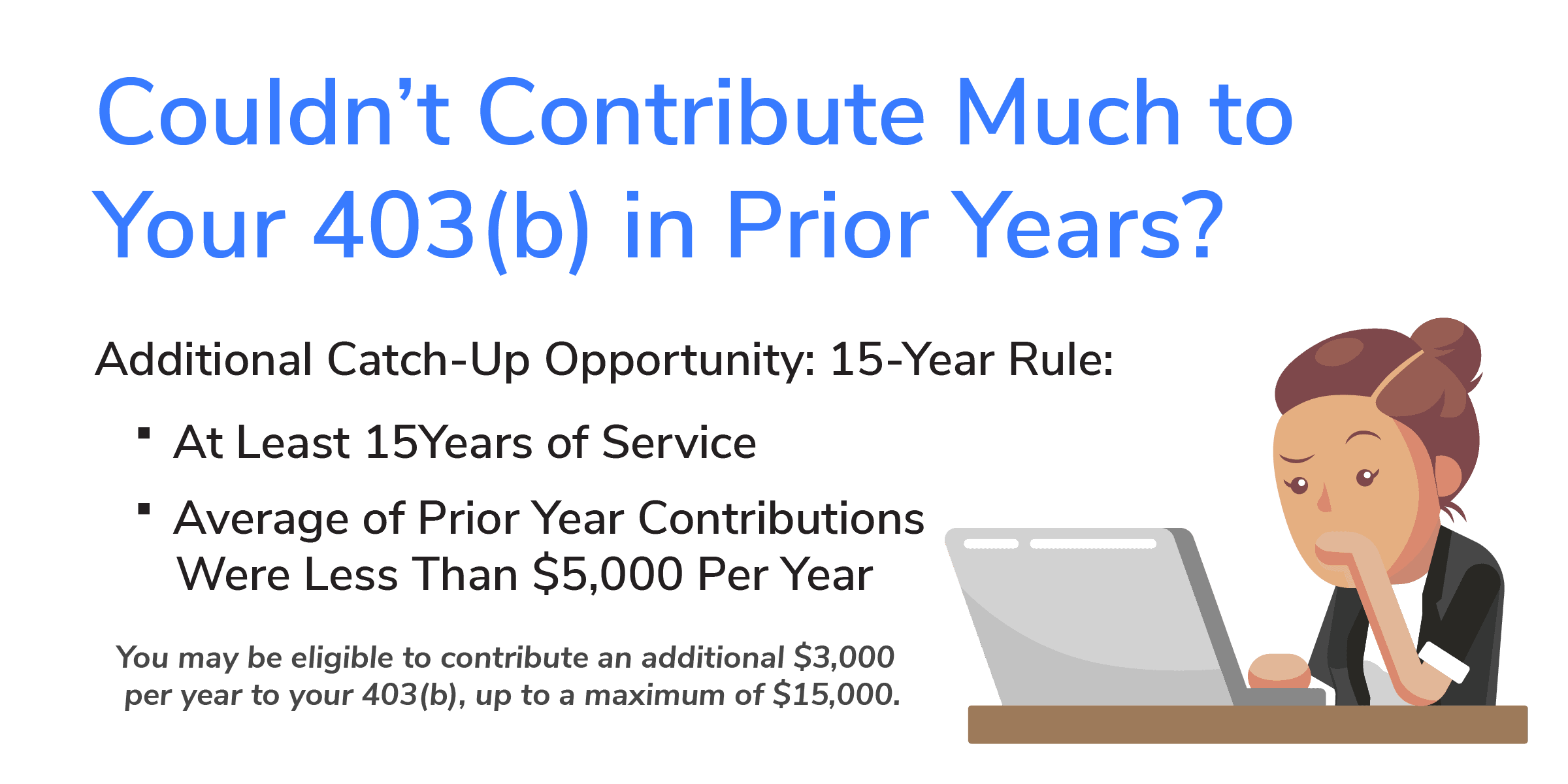

If you couldn’t contribute much to your 403(b) in prior years, your plan may offer you an additional catch-up opportunity. It’s called the 15-year rule, because it applies to workers with at least 15 years of service. If the average of your prior year contributions were less than $5,000 per year, you may be eligible to contribute an additional $3,000 per year to your 403(b), up to a maximum of $15,000.

Tax Benefits Available in Your 403(b)

There are different ways you can invest for retirement, but

your 403(b) should be your preferred option if only for the tax benefits.

Saving and investing through a 403(b) retirement plan account helps you manage your tax liability in two important ways. First, you contribute to your 403(b) account with pre-tax income.

In this world, nothing can be said to be certain except Death and Taxes.

Before the IRS takes their slice of your take-home pay, you can put some of it out of their reach (at least temporarily).

When the IRS does take their share of your earned income each year, they are taxing a smaller amount—your gross pay minus your 403(b) contribution. As a result, you end up paying less taxes on your current income.

The second way your 403(b) account helps you is through tax-deferred growth. When you receive gains and income from the investments in your 403(b), you won’t pay taxes on them right away. So more of the money you earn can be compounded to grow for the future. In a taxable investment account, this money would be taxed as ordinary income or capital gains.

You’ll notice we didn’t say anything about your 403(b) account being tax free, because it’s not. You will pay taxes on qualified withdrawals you make after age 59½ at your ordinary income tax rate. If you take money out of your 403(b) before age 59½, you may also pay a 10% early withdrawal penalty on top of ordinary income taxes.

A mutual fund is an investment that pools savings from different investors together to follow a common investment strategy (for example, value or growth investing) and seek a common investment objective (for example, long-term growth).

The idea behind a mutual fund is “strength in numbers” — you could invest on your own and buy several different stocks for your portfolio, but it would cost you a lot of money to do so. By pooling your assets together with investors who share the same goals, you can hire a professional money manager who makes buy and sell decisions on behalf of the fund.

There are thousands of mutual funds to choose from in the investment marketplace. Your 403b plan likely offers a select menu of funds that covers the major asset classes and investing styles, such as:

- Growth equity funds invest in stocks of fast-growing companies.

- Value equity funds invest in stocks that the fund manager thinks are underpriced relative to their potential for growth.

- Equity income funds invest in stocks of established companies that pay dividends to shareholders.

- Large-cap funds invest in stocks of the largest companies in the U.S.

- Small and mid-cap funds investing in smaller companies that have potential for explosive growth.

- International funds invest in stocks of companies outside of the U.S.

- Global funds invest in stocks from all countries, including the U.S.

- Emerging market equity funds invest in stocks of companies located in developing countries and economies.

- Sector funds invest in stocks of companies in specific industries.

- Bond funds invest in debt securities issued by companies.

- High yield funds invest in bonds of companies offering higher interest rates.

- Money market funds invest in short-term bonds offering low interest rates and relatively stable values.

- Asset Allocation funds offer the convenience of one-stop-shopping for investors looking for an easy solution for diversifying their investments.

Your 403(b) plan likely offers different ways to put your savings to work for your future. Having multiple options can be an advantage—you can design an investment plan around your specific goals or the way you like to invest.

However, having more choices also makes your investment decisions more complicated. Understanding the benefits of the different investment options available to you can help make this decision simpler for you.

There are too many plan variations to include in one guide. Below are the most common investment choices available using our preferred vendor Fidelity Investments.

Lifecycle Investment Options

Some asset allocation funds will invest and manage their assets to fit the needs of certain groups of investors. For target date funds, these investors are grouped by age or their planned retirement date. The target date fund will invest more aggressively when the time horizon is long, seeking to grow assets over the long term. As investors’ time horizon get shorter, the target date fund will shift its allocation to be less aggressive and seek to preserve investment values.

Certain funds also target investors by their risk profile. Target risk funds invest along a spectrum from conservative to aggressive, changing their allocation to suit specific investor risk profiles. For example, an investor may have a long-time horizon for retirement but not much tolerance for an aggressive investment strategy. This investor may prefer a target risk fund that invests in a way that suits a more conservative risk profile.

Core Investment Options: Passive vs. Active Funds:

Another simple solution for investors is to buy a mutual fund that tracks the performance of a stock market index—owning all stocks that are part of the index and seeking returns that are about equal to the index. Index funds are often less expensive than other funds because there really are no investment decisions for a manager to make—if a stock is part of an index, it’s also part of the fund portfolio. This is known as passive management.

While this “hands off” management style is simple to implement, returns of passive funds also don’t vary from the index. If the index or the broader market goes down, so does the value of the passive index fund.

An actively managed fund will try to beat the returns of an index or the broad market, and the portfolio manager can pick investments they believe will outperform (within the parameters of fund’s investment strategy) without being tied to a market index.

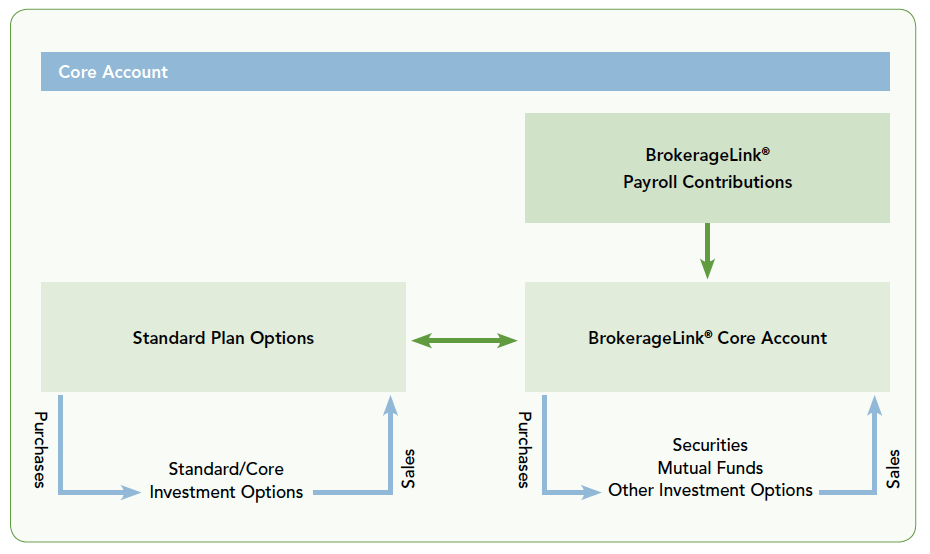

Your 403(b) may also offer a wider range of investments than what’s available in the standard menu of mutual funds and annuity options. In 403(b) plans through Fidelity, this option is called BrokerageLink®.

BrokerageLink® opens a window to a wider universe of investment options, including thousands of mutual funds and individual stocks and bonds. BrokerageLink® may be a good option if you’re an experienced investor and want to put your savings to work in options not currently available in your 403(b) plan lineup. You may also want to consider BrokerageLink® if you prefer your 403(b) account managed by an independent investment advisor.

It’s important to note your 403(b) plan may limit how much of your account may be invested through the BrokerageLink® window. Many plans require you to maintain a minimum balance in a fund from the standard investment menu, at least to cover fees charged by your 403(b) plan.

Risk is not something to be ignored but rather embraced so you can make rational decisions about your investments.

There are risks and costs to action. But they are far less than the long range risks of comfortable inaction.

The financial world has many ways to talk about risk—alpha, beta, Sharpe ratio and so on—but at the end of the day, how much do you, or frankly most financial professionals, really understand about these terms? The answer is: not much.

No one really understands risk, so investors don’t talk about it and the consequences are significant. Only one in four clients say their financial advisor has talked about how much their investments may decline if the market crashes, per an investor survey by FinMason, a financial technology firm.

People think about risk and reward trade-offs nearly every day, most often outside of the context of the investment markets.

Consider these choices:

- “Should I buy life insurance?” You weigh the risk of paying too much premium for a life policy, versus the reward of knowing your beneficiaries get some degree of financial protection.

- “What should my car insurance deductible be?” You may reward yourself with lower premiums by choosing a higher deductible, but you risk paying more out of pocket if you have an accident.

- “Should I go to the gym or stay on my couch?” You risk the poor health consequences of a sedentary lifestyle for the reward of easy entertainment.

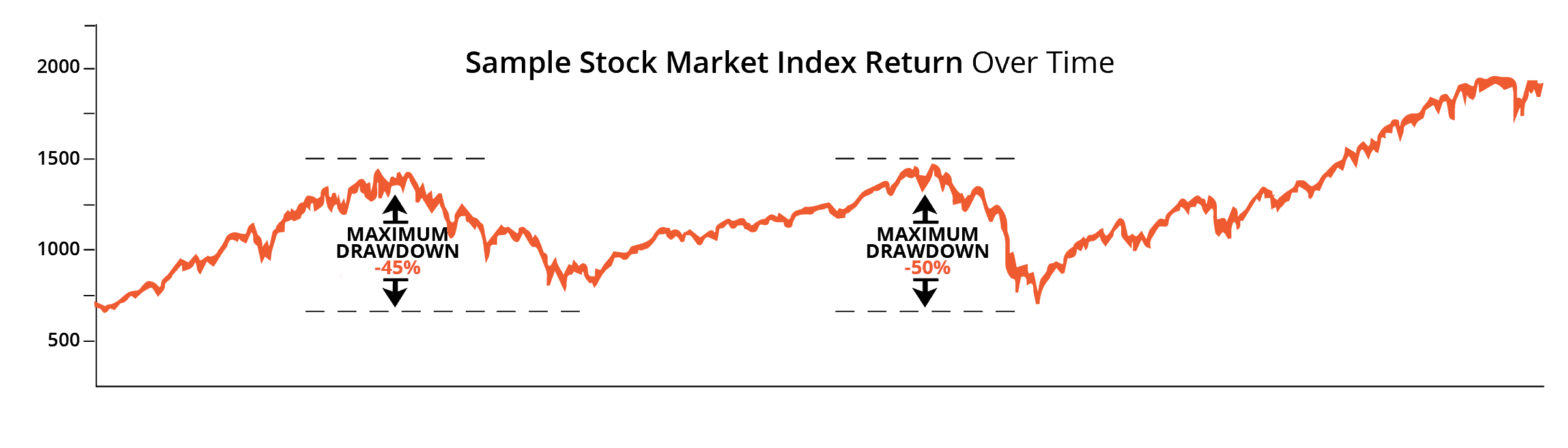

We think all the sophisticated ways to measure and discuss investment risk make the discussion more complicated. It needs to be kept simple. The one risk measurement you should care about the most (whether you realize it or not) is maximum drawdown risk—how much can you potentially lose in a catastrophic market downturn?

THESE TYPES OF DECLINES ARE WHAT YOU WANT TO AVOID:

This chart is for illustrative purposes only and must not be relied upon to make investment decisions.

To us, maximum drawdown is the only risk barometer that really matters, for two primary reasons: First, maximum drawdown is easy for investors to understand—it’s all about how much pain they are willing to endure to seek adequate returns.

Second, maximum drawdown can’t be changed, obscured, hidden or beautified by other performance statistics. With any peak-to-trough drop in investment value, what you see is what you get. There’s no hiding or smoothing over the consequences of a significant loss.

Investing is a marathon, not a sprint. It’s easy to get caught up in the latest hot stock, but the investors who survive and prosper are those who can manage their investment risk.

You should never invest in a product without first asking yourself “How much am I willing to lose?”

The Key Steps to Take Today to Supercharge Your 403(b) Account!

Now that you’ve learned more about the features of your 403(b) plan and your options for putting your savings to work, you should review your current investment plan. The first step is creating your investor profile.

Think of your profile as the story of your financial life—what it looks like today, and what you want it to look like in the future.

Your profile will be your guide as you set goals, pick investments and make changes along the way to retirement, and possibly even beyond that. You can start to write this story by asking these important questions:

1. How much will you need for retirement?

There’s a temptation to pick an arbitrary number as your ultimate investment goal—say, $1 million. But an arbitrary number with no thought behind it is not a goal worth achieving.

So where do you begin establishing a goal? You can start by looking at your current income and lifestyle. It is generally assumed you can maintain your current lifestyle in retirement on 80% of your current annual income. This is a good place to start, but you should adjust it based on what you want your retirement to be.

For instance, if you plan to travel during retirement or want to provide financial support to family members, you should use a higher percentage of your current annual income, even as much as 100%.

Also, if you’re just starting your career, you can assume your income is going to increase as you gain experience. Instead of using your current annual income to estimate your expected retirement income, you can go to a salary estimator web site to see the average salary for your profession or industry. You should also assume this salary will increase over time along with growth in the overall economy.

Once you estimate your annual retirement income needs, you can multiply this amount by the number of years you plan to spend in retirement. This can be tricky to estimate too. But you can use current life expectancy statistics and add a few years in the event you live a longer than average life. To be on the safe side, you should estimate to spend 30 years in retirement.

2. How much do you need to save with each paycheck?

Your savings rates or contributions are also personal decisions and will depend on your household budget. You should try to save something on a regular basis, and routine payroll deductions through your 403b can help you establish a good savings habit. Once you get started, you can increase your contributions over time.

You can also use any matching contributions from your employer as a guideline. Matching your 403b contributions is basically free money offered by your employer, so you should make the most of this benefit.

Usually, an employer will match up to a specific percentage of your contributions. For example, if your employer matches up to 6% of your contributions, you should at least contribute 6% from your paycheck to get all this free money.

Your employer may only match a portion of your contributions; for instance, 50 cents of every dollar you contribute. You should still contribute enough from your own salary to maximize this matching contribution.

Also keep in mind these matching contributions may come to you gradually, after you complete so many years of service. This is called vesting and it’s designed to encourage you to stay with your employer to claim this “free money” as yours.

3. How much risk are you willing to tolerate your investments?

The rate of return you make on your investments will depend on how much risk you’re willing to take. Period!

Most investment guides will ask you to pick a target rate of return on your investments. We disagree with this approach because the key to “sticking with” any investment is being able to tolerate the eventual decline in account values.

You should decide what is the maximum amount of loss you are willing to tolerate. From there you can work backwards to then find the best mix of investments to match your tolerance for risk.

If you’re just starting out and have many years until retirement, you may be able to tolerate more risk and therefore are able to utilize more aggressive investments. However, if you are approaching retirement your appetite for risk is much lower and therefore you are best suited to avoid aggressive investments.

4. What is your time horizon?

The first questions were all about money, but this one covers the other important component of investing—time.

Your time horizon is the number of years between now and your planned age of retirement. Everyone tends to use 65 as the default age of retirement, and this is a good benchmark to use to calculate your own time horizon.

Many people today want to work longer, beyond the typical retirement age of 65. Many more think they will have to work longer for the income. If it’s possible, it’s smart to delay your retirement if you can—it gives you more time to build your savings and contribute to Social Security as well.

But keep this reality in mind—the average age at which current retirees entered retirement is much lower than 65. You may not be able to work as long as you want to due to health factors. This would also lengthen the number of years you would need your retirement savings to last. All things to keep in mind as you craft your personal investor profile.

5. What’s your risk tolerance?

The standard spectrum of risk runs from conservative (risk averse) to aggressive (risk tolerant). Most likely, you’ll be somewhere in between.

Your risk tolerance is really a factor of your personality; if you’re comfortable taking more risk to seek greater returns, then you’re probably a more aggressive investor. If the thought of losing money in your retirement account would keep you awake at night, you’re likely more conservative in your investment approach.

The best way to learn more about your risk tolerance is to take a quiz. Many companies offer a risk tolerance questionnaire or risk profiling tool to help investors as part of the planning process. This questionnaire will ask you emotional questions related to money—how you feel about a drop in your investment value, for instance.

The answers you provide will help place your risk profile on the spectrum between conservative and aggressive. You can then use this profile as you consider investments for your portfolio or select an investment strategy to align with your comfort level with risk.

Sometimes, these profiles lead you directly to a strategy or portfolio that lines up with your personality. These recommendations can be helpful but be sure to consider other factors in your investor profile as you begin to carry out your investment plan.

How Potomac Can Help (Going At It Alone VS. Getting Help)

As you can see, you have a lot of options to consider as you plan to put your 403(b) money to work. It’s okay to feel overwhelmed by all the decisions you must make. But you also should know you don’t have to face these decisions entirely on your own, if you don’t want to.

What If You Want To Go It Alone?

- Review the fund and investment options available in your 403(b) lineup and pick a mix of investments that aligns with your goals.

- Diversify your portfolio with a broad range of fund types to manage market and investment risk.

- Monitor the market and adjust your portfolio if necessary.

- Take life changing events into consideration (e.g., college savings, recent grandchildren, illnesses, inheritance etc.) and adjust your retirement strategy accordingly.

How can a teacher or a healthcare worker–people who live and work under extreme demands on their time–be expected to know what to do with a list of investment choices provided without any guidance? Will they ever find time to do the required homework that helps them understand how they really feel about risk? Or how the investments in their portfolio may perform under certain market conditions?

Most 403(b) participants lack the time, knowledge and inclination to study all the options available to them. So, it remains likely that many will make the wrong choice for their investment profile and risk tolerance.

In addition, it takes even more time to monitor the market, respond the market changes and continue to keep investment selections aligned with retirement goals regardless of personal or market changes.

The current lineup of 403(b) investing options woefully underserves teachers, doctors and nurses—a few of our country’s most important professions.

Plans are filled with underperforming funds, complex rules meant to confuse participants into inaction, and annuities not suitable for anyone’s long-term financial goals except for the product provider who issues them. We are here to change that!

At Potomac Fund Management, we help you understand your 403b plan and how to navigate its plan options, so you can feel confident you’re making the right financial decisions for your situation.

Potomac has been managing client assets since 1987. We specialize in helping teachers, doctors and nurses like you select the right funds to match your risk preference and financial goals.

Knowing Your Tolerance for Risk Gets Your Closer to Protecting Your Investments

How we get to know you:

To get the right answers you must ask the right questions! We get to know your true risk tolerance by discussing your goals, financial situation and how low your investments can go before you feel uncomfortable.

How we put together a plan:

We analyze your current holdings and make a recommendation based on your tolerance for risk. If you aren’t sure if your current investments align with your risk tolerance, take our questionnaire for a free analysis.

Once we get a better understanding of your tolerance for risk we then build strategies designed to help you invest in a way that helps you reach your financial goals while also protecting you from extreme losses.

Step-By-Step Process:

- Complete a risk questionnaire.

- Verify if your current holdings match your tolerance for risk.

- Have a call with a Potomac financial advisor to discuss your custom needs and develop a plan.

- Turn over investment management duties to Potomac so you can go enjoy life!